Executive summary

2025 is a transitional year for server CPUs: x86 incumbents (Intel and AMD) remain the backbone of most enterprise racks while Arm-based designs (hyperscaler custom chips and third-party Arm vendors) continue to gain strategic traction — particularly for energy-efficient and AI-oriented workloads. Market revenue is growing modestly (single- to mid-digit CAGR), but structural change — driven by AI acceleration, hyperscaler custom silicon, and rack-scale solutions — is reshaping vendor share, product segmentation, and the flow of retired hardware into the second-hand channel. This briefing summarizes market size estimates, competitive positioning, technology trends, investment implications, and short-to-medium-term effects on the used/server resale market.

Market size & growth

- According to Precedence Research, the global data center / server CPU market is estimated at USD 14.19 billion in 2025, with a projected increase to ~USD 28.04 billion by 2034 (CAGR ~7.87 %) [1].

- Future Market Insights similarly estimates the 2025 base at USD 14.15 billion and forecasts growth to USD 30 billion by 2035, with a ~7.8 % CAGR over that period [2].

- For the broader IT Asset Disposition (ITAD) / remarketing space, Precedence Research projects the global ITAD market to reach USD 90.06 billion by 2034, up from ~USD 29.23 billion in 2025 (CAGR ~13.32 %) [3].

- Other ITAD projections: The Business Research Company estimates the ITAD market will grow from USD 19.13 billion in 2024 to USD 20.65 billion in 2025 and further to USD 31.58 billion by 2029 (CAGR ~11.2 %) [4].

- IMARC estimates the global ITAD market (all asset types) was USD 18.02 billion in 2024 and will reach ~USD 34.31 billion by 2033 (CAGR ~7.05 %) [5].

Thus, the verified data suggests:

- The server CPU market is in the low-teens (USD billions) in 2025, not “tens of billions” in a large sense, but with solid growth potential.

- The ITAD / secondary hardware disposal / remarketing market is sizable and growing, though its growth rate and size depend on scope (servers, desktops, memory, etc.).

Competitive landscape

- Intel (x86) — Intel still maintains substantial share in enterprise server deployments and is often perceived as the “default” in many legacy workloads. A recent article in Network World notes that Intel continues to “retain server, client market share lead over AMD” in 2025 [6].

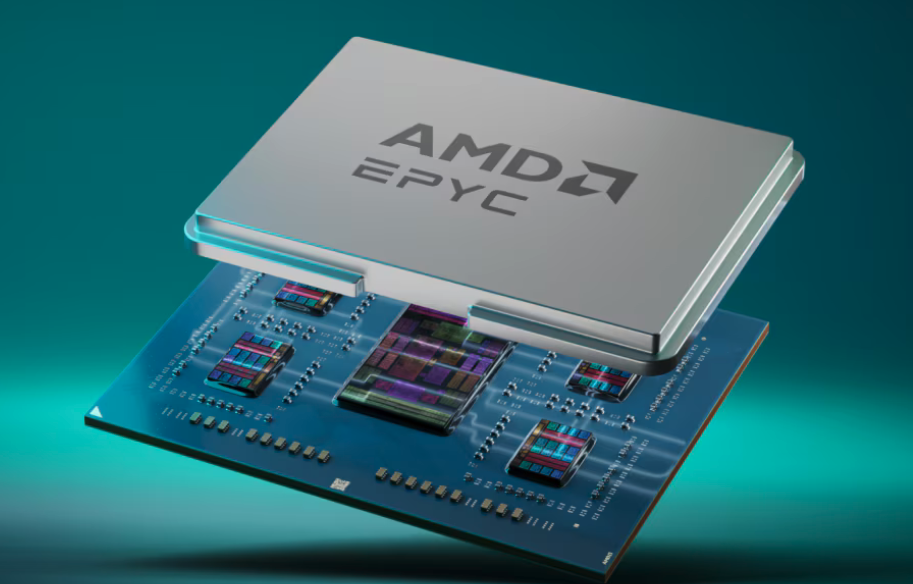

- AMD (x86 EPYC) — AMD’s data center segment revenue (which includes both CPU and GPU) for Q1 2025 was USD 3.7 billion; estimates attribute a substantial portion of that to server CPU sales (USD 2.5–3 billion) [7]. This supports AMD’s stronger momentum in data center infrastructure.

- Arm / non-x86 vendors — There is credible industry commentary that Arm / alternative architectures are gaining share in the data center space. For example, a SemiEngineering article describes a shifting dominance toward AMD and Arm in data center CPUs [8]. However, precise 2025 share numbers (e.g. “15–25 %”) are not reliably confirmed by published data I found.

Technology & demand drivers

These are strategic drivers and less amenable to precise numeric verification, but broadly accepted in industry discourse:

- AI acceleration & co-design: CPU + GPU / accelerator integration is becoming increasingly important in designing data center racks, especially for inference/training workloads.

- Energy efficiency & TCO pressure: Hyperscalers and cloud providers emphasize performance per watt; architectures that improve energy efficiency gain favor.

- Workload specialization: Different CPU classes (control plane, management, inference orchestration, storage) are emerging rather than one-size-fits-all.

- Platform transitions: DDR5, PCIe Gen 5/6, interconnects and memory bandwidth push new generation hardware demand cycles.

Effect on the second-hand / ITAD market

Based on verified data and plausible extrapolation:

- Increased supply of retired hardware — As enterprises and cloud providers upgrade to newer CPU generations or hybrid AI infrastructures, older server CPUs and servers will flow into the second-hand market.

- Value differentiation — Used CPUs and servers with newer standards (DDR5, PCIe Gen4/5) or validated compatibility for AI workloads will command higher prices.

- Role of certified refurbishers / ITAD providers — Value recovery, refurbishment, warranty and data-sanitization will be key differentiators in the secondary market.

- Growth in ITAD / remarketing infrastructure — Given the size and growth forecasts of the ITAD market [3][4][5], the infrastructure (logistics, testing, resale channels) for used server hardware will scale.

- Price compression for older commodity units — As supply increases and demand is selective, older generation CPUs will see downward price pressure.

Investment & business implications

- Investors should favor firms in AI infrastructure (hybrid CPU + accelerator), data center refresh cycles, and ITAD / reuse platforms.

- OEMs / server integrators should lean into modular, rack-scale or heterogeneous designs and provide servicing/lifecycle support.

- IT asset holders / enterprise data centers should evaluate the opportunity to monetize retired assets via certified partners.

- Resellers / refurbishers should invest in testing, certification, warranty services, and targeted channels for high-value used hardware (e.g. with GPU-pairing capability).

Risks & watch indicators

- Hyperscalers increasing in-house chip design (reducing third-party CPU demand).

- Rapid platform transitions (e.g. memory, interconnect) making “recent” hardware obsolete faster.

- Geopolitical constraints disrupting supply chains.

- Dominance of GPU-first architectures altering CPU demand patterns (though CPUs remain essential for orchestration).

The 2025 server CPU market is moderately sized but in structural transformation.

While Intel and AMD remain central players, Arm / alternative architectures are rising in influence.

This shift, coupled with accelerating refresh cycles, will feed into a growing second-hand market ecosystem, offering opportunities for value recovery and efficiency.

Acknowledgment:

This report was prepared with insights and market experience contributed by BuySellRam.com, a trusted ITAD and computer hardware company. Here are some of their services: Sell GPU | Sell CPU | Sell SSD

References:

- Precedence Research, Data Center CPU Market Size & Forecast 2025 to 2034 — global data center CPU market = USD 14.19 billion in 2025 and forecast to USD 28.04 billion by 2034 (CAGR ~7.87 %)

- Future Market Insights, Data Center CPU Market 2025–2035 — base 2025 estimate USD 14.15 billion, CAGR ~7.8 % to 2035

- Precedence Research, IT Asset Disposition Market Forecast 2025 to 2034 — global ITAD projected ~USD 90.06 billion in 2034 from ~USD 29.23 billion in 2025 (CAGR ~13.32 %) [source]

- The Business Research Company, IT Asset Disposition Global Market Report 2025 — ITAD market from USD 19.13 billion in 2024 to USD 20.65 billion in 2025, and to USD 31.58 billion in 2029 (CAGR ~11.2 %)

- IMARC Group, IT Asset Disposition Market 2025–2033 — global ITAD ~USD 18.02 billion in 2024, forecast to ~USD 34.31 billion in 2033 (CAGR ~7.05 %) [source]

- Network World, “Despite the hubbub, Intel is holding onto server market share” (2025) — Intel continues to retain server/client market share over AMD [source]

- SemiEngineering, “Data Center CPU Dominance Is Shifting to AMD and Arm” — data center revenue breakdown and market dynamics [source]